To print a customer statement, click menu Ledgers > Sales > Reports > Statements.

From here you can print a statement for a singleCustomer, a range or all Customers.

Within View > Parameters > Sales you can edit messages relating to overdue accounts which are automatically added depending on the age of the debt. You can change these messages as often as you like.

You may wish to add other messages occasionally – special offers, advising of shutdowns etc. These can be added through the stationery layout – File Menu > stationery design > sales ledger and daybooks > statements – this will allow you to add images as well as text.

If you do not wish all customers to receive the messages use the stationery tabs in the customer maintenance and create a conditional ‘Print when’ in the stationery design.

How Do I Deal With Prompt Payment Discounts?

Many businesses offer customers a discount if they pay their invoices early.

Prior to 1st April 2015 when you offered a prompt payment discount you should have charged V.A.T. only on the discounted amount, even if the customer didn’t take advantage of the prompt payment discount offer. However on 1st April 2015 HMRC changed the rules and VAT is now payable on the amount received.

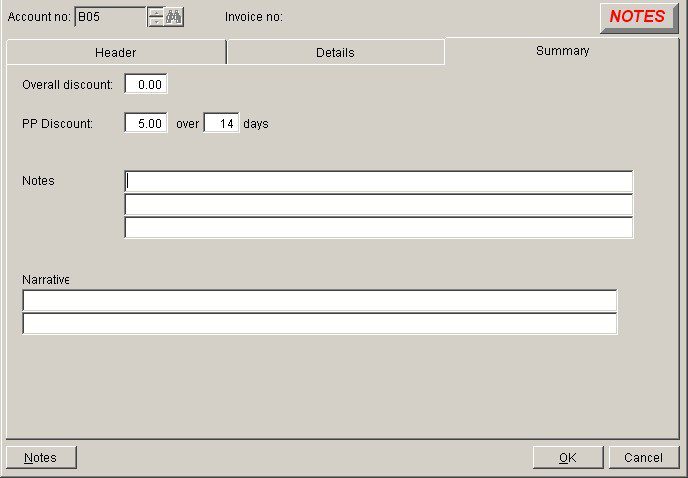

The invoicing part hasn’t changed and is shown here: Add the overall prompt payment discount percentage and period in days to the summary of your invoice like this:

You may need to update your stationery design to include the discount and period in your invoice footer – see Design Your Stationery.

Customer Receipt

When the customer pays you need to check whether he has paid the discounted amount within the time allowed. If he has then simply record the receipt as is and allocate the receipt as normal.

If the receipt is outside the terms you need to decide whether to request the difference – by invoice – discount + VAT.

If the customer has paid the full amount as he was late in paying you will need to split the payment – match the amount paid to the customer’s account and post the difference as a VAT inclusive nominal receipt extracting the VAT and posting the balance to the appropriate sales account.

This process applies to supplier invoices too. When invoices are received post them at full value. When paying, deduct the discount and post to the discount account. That discount will include VAT. Each month determine the amount of discount for the month and transfer the VAT element to the VAT account – It’s probably best to create a dummy purchase ledger account.

Payment: Dr. Supplier Acccount – Full amount Cr. Dummy P/L Discount Cr. Cash Book Net Amount paid.

Monthly: Dr. Dummy P/L Discount account with full amount by credit note( splitting out VAT element) Cr. Discount Received acccount – Net and Cr. VAT account.

How Do I Write Off A Bad Debt?

Please make yourself aware of the HMRC rules relating to how soon you can write off a bad debt.

Write off a bad debt by producing an internal credit note for the amount being written off. SeeCredit a Customer Account.

The V.A.T. analysis must be the same as the invoice(s) being written off – i.e. use the same V.A.T. codes (and rates) and net amounts. Use the Daybooks > Sales> Credit a Produced Invoice facility to be sure you are reversing the VAT correctly. You can change the nominal code to bad debt write off or provision account before posting.

Consider whether the amount is a bad debt or uncollectable for some other reason – i.e. the goods never arrived – in which case no sale was made – in this sort of case you can immediately credit the sales account and VAT and send the credit to the customer.

Otherwise, at the appropriate time, charge the net amount to bad debt expense account and debit the VAT account.

Allocate the credit note against the invoice(s).

How Do I Record A Contra?

Quite a lot of businesses have customers who are also suppliers – It is not uncommon for a supplier who is owed more by the customer than he owes to agree to a contra so that the customer pays only the net value and the supplier does not need to make a payment. The reverse situation also applies.

There are two ways of dealing with this scenario –

The supplier can post a supplier payment and a customer receipt when he receives the net amount.

The supplier posts a receipt for the received amount into his sales ledger and creates a contra entry for the balance on the purchase ledger. The contra is made through Ledgers > Nominal > Journals > Standard and a debit is made to the purchase ledger and a credit to the sales ledger. You will then need to allocate the journals made to both the sales and purchase ledgers to the invoices settled.

You may need to agree with the other party which invoices have been settled before posting the contra.

Where no payment has been made but a contra is necessary – e.g in the scenario above both options are still available as the postings through the cash book come back to Nil. Alternatively just raise a journal to both sales and purchase ledgers.